IDAs are part of the Single Intraday Coupling (SIDC), where hybrid implicit capacity allocation is now possible. In the continuous market segment, the capacity is allocated using the continuous trading method on a first-come, first-served basis. The Intraday Auctions follow the same principles for allocation of capacities as trading on the Day-Ahead market and are allocated through implicit auctions in IDAs to harmonize calculation and distribution on the intraday market. The pricing of intraday cross-border capacities reflects their shortage at a specific time and sends appropriate price signals to the market.

Before executing trades, market participants submit their orders to their respective NEMO. These orders are then collected and processed by EUPHEMIA, the algorithm used for both SDAC and IDAs. EUPHEMIA determines which orders should be executed and which should be rejected.

Trading is available in 15 min Market Time Unit products.

Cross-zonal capacities cannot be allocated simultaneously for IDAs and for Continuous trading along the same borders. Therefore, cross-zonal capacity allocation within the continuous SIDC is suspended for a limited period during which the cross-zonal capacities are available for allocation in the Intraday Auctions.

20 minutes before each IDA, the cross-border allocation on SIDC Continuous Trading is suspended for 40 minutes.

Under normal circumstances, IDA publishes the Final Market Results 20 minutes after the Orderbook Gate Closure Time.

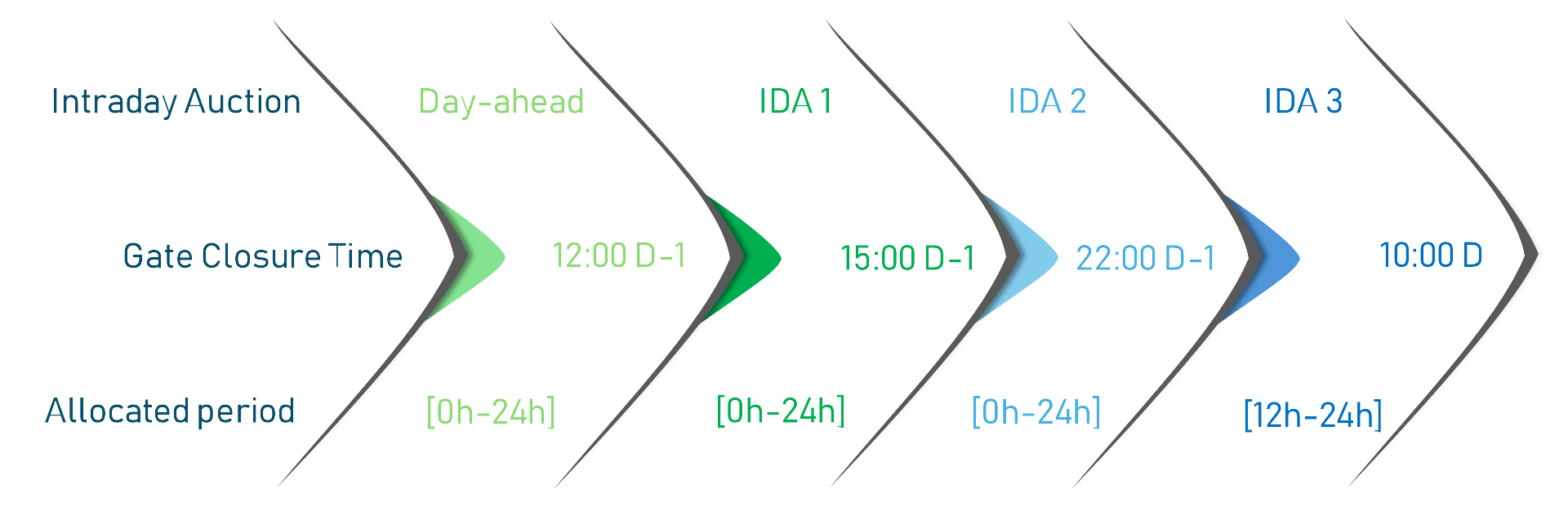

After the Day-ahead auction, three IDAs follow.